Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

August 18, 2025 11:41 AM

Credit cards keep business moving—until someone else starts using them without permission.

Whether it’s a stolen card, a hacked account, or charges you never authorized, credit card fraud is more common than most people think and more disruptive than you might expect. It affects businesses of all sizes, with consequences that range from lost revenue to broken trust with customers, vendors, and partners.

Even the most organized teams can get blindsided. And it’s because fraud often starts quietly. A strange charge here. A flagged transaction there. But those small warning signs can snowball fast, creating bigger financial and operational headaches if they go unchecked.

And it’s only becoming more common. In 2024 alone, 62 million Americans experienced some form of credit card fraud, totaling more than $6.2 billion in unauthorized purchases.

It’s truly not a matter of if you’ll be impacted, but when.

In this blog post, I’ll share what to watch out for, how to stay ahead of potential fraud, and the modern business tools that can help make prevention easier and a lot more effective.

Credit card fraud can take many forms, but most cases fall into a handful of well-known tactics. Knowing what these look like is the first step toward spotting and stopping them early.

1. Physical card theft

This is the most straightforward type of fraud: someone gets hold of the actual credit card and uses it to make unauthorized purchases. It can happen through a lost or stolen wallet, sharing credit cards among teams, or even cards intercepted in the mail.

2. Card-not-present fraud

In this case, the thief doesn’t need the physical card, just the numbers. Online and phone transactions are especially vulnerable, since they rely on sharing the card details. If the card number is compromised in a data breach or phishing attack, it can be used in these scenarios without ever having to touch the card itself.

3. Account takeover

Here, fraudsters gain access to the company’s credit card account by manipulating personal or business information, like login credentials, billing addresses, or even employee details. Once inside, they can change passwords and account settings, reroute cards, or quietly rack up charges under your business’s name.

4. Application fraud

This type of fraud involves someone using stolen business details, like tax IDs, addresses, or employee information, to open entirely new credit card accounts. It’s especially dangerous because it can go undetected until bills show up or credit limits are maxed out.

5. Cloning and skimming

If employees use cards at gas stations, ATMs, or point-of-sale systems, they could encounter card skimmers, which are small devices that capture magnetic stripe data. That data can then be cloned and used to make fraudulent purchases elsewhere, often before anyone notices.

6. Data breaches

Sometimes the risk isn’t internal. A vendor, platform, or payment processor your business works with might go through a breach, exposing your company’s card numbers or associated employee info. These breaches often feed larger fraud schemes, especially in card-not-present scenarios.

Each method looks a bit different, but the end result is the same: unauthorized access to your credit card account, often without you even realizing it until the damage is done.

You’re likely thinking about the money lost when credit card fraud hits. But the real cost goes far beyond a few unauthorized charges.

Even if you catch the fraud and get reimbursed, there’s often a lag that can create real problems. You may end up covering lost inventory, paying higher interest, or dealing with issuer fees. And let’s not forget chargebacks, which hit hard when you’re already working to manage cash flow.

Fraud doesn’t just drain money, but time. The minute something suspicious happens, you’re pulling in finance, operations, maybe even IT. Teams lose access to cards, vendor payments get held up, and someone has to piece it all back together. That’s time that could’ve been spent on higher-value work.

Trust matters. A missed payment, or even the impression that your systems aren’t secure, can put vendor relationships at risk or stall important projects. It introduces friction at a time when you need things to run smoothly.

There’s a mental load, too. Investigating fraud, reissuing cards, updating payment methods across platforms and vendors—it all adds up. For lean finance teams, it’s a heavy lift on top of everything else they’re already juggling.

The earlier you catch fraud, the easier it’ll be to contain the damage. Here are a few warning signs that something might be off:

Manual reviews aren’t enough. To catch issues early, businesses need to layer in tools that offer real-time visibility:

Building these habits into your monthly rhythm can make fraud detection feel less like a scramble and more like part of the process.

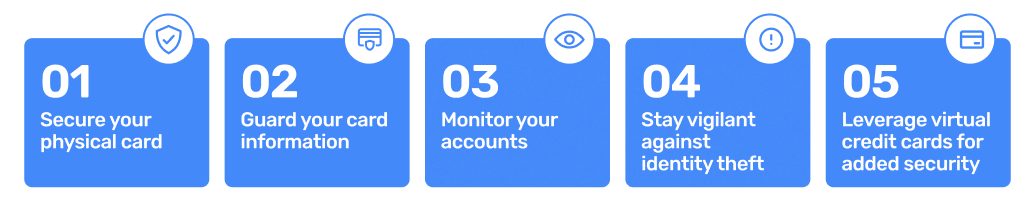

Follow these five practical steps to prevent fraud:

1. Secure your physical card

It sounds basic, but it matters. Make sure company cards are stored safely, especially when traveling or shipping them to employees. Avoid sharing cards across teams whenever possible too, because what might feel convenient at first can quickly become a point of vulnerability.

2. Guard your credit card information

Stick to secure, trusted websites when entering payment details, and avoid public Wi-Fi for financial transactions. If you can, don’t store card numbers in retailer profiles or software tools. It’s one less place your data can be compromised.

3. Monitor your accounts

Set up alerts for every transaction, or at least those over a certain threshold. It’s one of the easiest ways to flag unexpected activity fast. Then, make account reviews part of your weekly or monthly close process, not just something you check when something seems off.

4. Stay vigilant against identity theft

Unsolicited calls, emails, or texts asking for sensitive business information should always raise a red flag. Use strong, unique passwords for all financial platforms, and enable multi-factor authentication wherever it’s available.

5. Leverage solutions like virtual credit cards for added security

Virtual cards are one of the most effective ways to reduce risk that comes with physical cards, especially in card-not-present transactions. They let you set spend limits, expiration dates, and vendor-specific usage rules, so even if card details are exposed, the damage is contained and minimal.

Virtual cards offer a simple but powerful way to reduce fraud risk, especially if you manage multiple users, vendors, and recurring payments in your business. Unlike physical cards, virtual cards are generated digitally and come with built-in controls that make them harder to misuse.

Here’s what makes them more secure:

Here are a couple of common ways you can use virtual cards in your business:

Even with the right safeguards in place, fraud can still happen. The key is acting quickly to limit the fallout and prevent it from happening again.

1. Contact your card issuer immediately

Report any suspicious activity and ask them to freeze or close the compromised card. Many issuers can reissue a new number on the spot and help reverse unauthorized charges. The faster you act, the less damage fraudsters can do.

2. Notify the credit bureaus

Place a fraud alert with the major credit bureaus—Experian, Equifax, and TransUnion. This flags your business credit profile and adds an extra layer of verification if someone tries to open a new account using your information.

3. Report the fraud to the FTC

You can file a report with the Federal Trade Commission. If the fraud involves a data breach, phishing scam, or impersonation attempt, this helps build a paper trail and supports broader investigations.

4. File a police report if needed

For large losses or clear cases of identity theft, you may also want to contact local law enforcement. This is especially important if a vendor or internal party is involved.

5. Take steps to prevent it from happening again

Spend & expense management tools that allow you to create virtual credit cards can help you build better controls going forward. By using virtual cards instead of traditional cards, it’ll be much easier to avoid the risk that comes with card sharing.

In my experience, the best protection isn’t reactive, it’s embedded into the tools teams use every day. That’s where Extend stands out for safer spend and expense management.

Even better: Extend works with the business credit card you already have. No need to switch banks or disrupt reward programs to get started, just more security and fewer manual steps.

Moral of the story: Fraud doesn’t just impact your bottom line, it disrupts your team, your operations, and your peace of mind. The more you understand how it works, the better prepared you’ll be to stop it before it spreads.

With the right habits and tools, you can protect your business and keep spending secure.

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Credit cards keep business moving—until someone else starts using them without permission.

Whether it’s a stolen card, a hacked account, or charges you never authorized, credit card fraud is more common than most people think and more disruptive than you might expect. It affects businesses of all sizes, with consequences that range from lost revenue to broken trust with customers, vendors, and partners.

Even the most organized teams can get blindsided. And it’s because fraud often starts quietly. A strange charge here. A flagged transaction there. But those small warning signs can snowball fast, creating bigger financial and operational headaches if they go unchecked.

And it’s only becoming more common. In 2024 alone, 62 million Americans experienced some form of credit card fraud, totaling more than $6.2 billion in unauthorized purchases.

It’s truly not a matter of if you’ll be impacted, but when.

In this blog post, I’ll share what to watch out for, how to stay ahead of potential fraud, and the modern business tools that can help make prevention easier and a lot more effective.

Credit card fraud can take many forms, but most cases fall into a handful of well-known tactics. Knowing what these look like is the first step toward spotting and stopping them early.

1. Physical card theft

This is the most straightforward type of fraud: someone gets hold of the actual credit card and uses it to make unauthorized purchases. It can happen through a lost or stolen wallet, sharing credit cards among teams, or even cards intercepted in the mail.

2. Card-not-present fraud

In this case, the thief doesn’t need the physical card, just the numbers. Online and phone transactions are especially vulnerable, since they rely on sharing the card details. If the card number is compromised in a data breach or phishing attack, it can be used in these scenarios without ever having to touch the card itself.

3. Account takeover

Here, fraudsters gain access to the company’s credit card account by manipulating personal or business information, like login credentials, billing addresses, or even employee details. Once inside, they can change passwords and account settings, reroute cards, or quietly rack up charges under your business’s name.

4. Application fraud

This type of fraud involves someone using stolen business details, like tax IDs, addresses, or employee information, to open entirely new credit card accounts. It’s especially dangerous because it can go undetected until bills show up or credit limits are maxed out.

5. Cloning and skimming

If employees use cards at gas stations, ATMs, or point-of-sale systems, they could encounter card skimmers, which are small devices that capture magnetic stripe data. That data can then be cloned and used to make fraudulent purchases elsewhere, often before anyone notices.

6. Data breaches

Sometimes the risk isn’t internal. A vendor, platform, or payment processor your business works with might go through a breach, exposing your company’s card numbers or associated employee info. These breaches often feed larger fraud schemes, especially in card-not-present scenarios.

Each method looks a bit different, but the end result is the same: unauthorized access to your credit card account, often without you even realizing it until the damage is done.

You’re likely thinking about the money lost when credit card fraud hits. But the real cost goes far beyond a few unauthorized charges.

Even if you catch the fraud and get reimbursed, there’s often a lag that can create real problems. You may end up covering lost inventory, paying higher interest, or dealing with issuer fees. And let’s not forget chargebacks, which hit hard when you’re already working to manage cash flow.

Fraud doesn’t just drain money, but time. The minute something suspicious happens, you’re pulling in finance, operations, maybe even IT. Teams lose access to cards, vendor payments get held up, and someone has to piece it all back together. That’s time that could’ve been spent on higher-value work.

Trust matters. A missed payment, or even the impression that your systems aren’t secure, can put vendor relationships at risk or stall important projects. It introduces friction at a time when you need things to run smoothly.

There’s a mental load, too. Investigating fraud, reissuing cards, updating payment methods across platforms and vendors—it all adds up. For lean finance teams, it’s a heavy lift on top of everything else they’re already juggling.

The earlier you catch fraud, the easier it’ll be to contain the damage. Here are a few warning signs that something might be off:

Manual reviews aren’t enough. To catch issues early, businesses need to layer in tools that offer real-time visibility:

Building these habits into your monthly rhythm can make fraud detection feel less like a scramble and more like part of the process.

Follow these five practical steps to prevent fraud:

1. Secure your physical card

It sounds basic, but it matters. Make sure company cards are stored safely, especially when traveling or shipping them to employees. Avoid sharing cards across teams whenever possible too, because what might feel convenient at first can quickly become a point of vulnerability.

2. Guard your credit card information

Stick to secure, trusted websites when entering payment details, and avoid public Wi-Fi for financial transactions. If you can, don’t store card numbers in retailer profiles or software tools. It’s one less place your data can be compromised.

3. Monitor your accounts

Set up alerts for every transaction, or at least those over a certain threshold. It’s one of the easiest ways to flag unexpected activity fast. Then, make account reviews part of your weekly or monthly close process, not just something you check when something seems off.

4. Stay vigilant against identity theft

Unsolicited calls, emails, or texts asking for sensitive business information should always raise a red flag. Use strong, unique passwords for all financial platforms, and enable multi-factor authentication wherever it’s available.

5. Leverage solutions like virtual credit cards for added security

Virtual cards are one of the most effective ways to reduce risk that comes with physical cards, especially in card-not-present transactions. They let you set spend limits, expiration dates, and vendor-specific usage rules, so even if card details are exposed, the damage is contained and minimal.

Virtual cards offer a simple but powerful way to reduce fraud risk, especially if you manage multiple users, vendors, and recurring payments in your business. Unlike physical cards, virtual cards are generated digitally and come with built-in controls that make them harder to misuse.

Here’s what makes them more secure:

Here are a couple of common ways you can use virtual cards in your business:

Even with the right safeguards in place, fraud can still happen. The key is acting quickly to limit the fallout and prevent it from happening again.

1. Contact your card issuer immediately

Report any suspicious activity and ask them to freeze or close the compromised card. Many issuers can reissue a new number on the spot and help reverse unauthorized charges. The faster you act, the less damage fraudsters can do.

2. Notify the credit bureaus

Place a fraud alert with the major credit bureaus—Experian, Equifax, and TransUnion. This flags your business credit profile and adds an extra layer of verification if someone tries to open a new account using your information.

3. Report the fraud to the FTC

You can file a report with the Federal Trade Commission. If the fraud involves a data breach, phishing scam, or impersonation attempt, this helps build a paper trail and supports broader investigations.

4. File a police report if needed

For large losses or clear cases of identity theft, you may also want to contact local law enforcement. This is especially important if a vendor or internal party is involved.

5. Take steps to prevent it from happening again

Spend & expense management tools that allow you to create virtual credit cards can help you build better controls going forward. By using virtual cards instead of traditional cards, it’ll be much easier to avoid the risk that comes with card sharing.

In my experience, the best protection isn’t reactive, it’s embedded into the tools teams use every day. That’s where Extend stands out for safer spend and expense management.

Even better: Extend works with the business credit card you already have. No need to switch banks or disrupt reward programs to get started, just more security and fewer manual steps.

Moral of the story: Fraud doesn’t just impact your bottom line, it disrupts your team, your operations, and your peace of mind. The more you understand how it works, the better prepared you’ll be to stop it before it spreads.

With the right habits and tools, you can protect your business and keep spending secure.

Credit cards keep business moving—until someone else starts using them without permission.

Whether it’s a stolen card, a hacked account, or charges you never authorized, credit card fraud is more common than most people think and more disruptive than you might expect. It affects businesses of all sizes, with consequences that range from lost revenue to broken trust with customers, vendors, and partners.

Even the most organized teams can get blindsided. And it’s because fraud often starts quietly. A strange charge here. A flagged transaction there. But those small warning signs can snowball fast, creating bigger financial and operational headaches if they go unchecked.

And it’s only becoming more common. In 2024 alone, 62 million Americans experienced some form of credit card fraud, totaling more than $6.2 billion in unauthorized purchases.

It’s truly not a matter of if you’ll be impacted, but when.

In this blog post, I’ll share what to watch out for, how to stay ahead of potential fraud, and the modern business tools that can help make prevention easier and a lot more effective.

Credit card fraud can take many forms, but most cases fall into a handful of well-known tactics. Knowing what these look like is the first step toward spotting and stopping them early.

1. Physical card theft

This is the most straightforward type of fraud: someone gets hold of the actual credit card and uses it to make unauthorized purchases. It can happen through a lost or stolen wallet, sharing credit cards among teams, or even cards intercepted in the mail.

2. Card-not-present fraud

In this case, the thief doesn’t need the physical card, just the numbers. Online and phone transactions are especially vulnerable, since they rely on sharing the card details. If the card number is compromised in a data breach or phishing attack, it can be used in these scenarios without ever having to touch the card itself.

3. Account takeover

Here, fraudsters gain access to the company’s credit card account by manipulating personal or business information, like login credentials, billing addresses, or even employee details. Once inside, they can change passwords and account settings, reroute cards, or quietly rack up charges under your business’s name.

4. Application fraud

This type of fraud involves someone using stolen business details, like tax IDs, addresses, or employee information, to open entirely new credit card accounts. It’s especially dangerous because it can go undetected until bills show up or credit limits are maxed out.

5. Cloning and skimming

If employees use cards at gas stations, ATMs, or point-of-sale systems, they could encounter card skimmers, which are small devices that capture magnetic stripe data. That data can then be cloned and used to make fraudulent purchases elsewhere, often before anyone notices.

6. Data breaches

Sometimes the risk isn’t internal. A vendor, platform, or payment processor your business works with might go through a breach, exposing your company’s card numbers or associated employee info. These breaches often feed larger fraud schemes, especially in card-not-present scenarios.

Each method looks a bit different, but the end result is the same: unauthorized access to your credit card account, often without you even realizing it until the damage is done.

You’re likely thinking about the money lost when credit card fraud hits. But the real cost goes far beyond a few unauthorized charges.

Even if you catch the fraud and get reimbursed, there’s often a lag that can create real problems. You may end up covering lost inventory, paying higher interest, or dealing with issuer fees. And let’s not forget chargebacks, which hit hard when you’re already working to manage cash flow.

Fraud doesn’t just drain money, but time. The minute something suspicious happens, you’re pulling in finance, operations, maybe even IT. Teams lose access to cards, vendor payments get held up, and someone has to piece it all back together. That’s time that could’ve been spent on higher-value work.

Trust matters. A missed payment, or even the impression that your systems aren’t secure, can put vendor relationships at risk or stall important projects. It introduces friction at a time when you need things to run smoothly.

There’s a mental load, too. Investigating fraud, reissuing cards, updating payment methods across platforms and vendors—it all adds up. For lean finance teams, it’s a heavy lift on top of everything else they’re already juggling.

The earlier you catch fraud, the easier it’ll be to contain the damage. Here are a few warning signs that something might be off:

Manual reviews aren’t enough. To catch issues early, businesses need to layer in tools that offer real-time visibility:

Building these habits into your monthly rhythm can make fraud detection feel less like a scramble and more like part of the process.

Follow these five practical steps to prevent fraud:

1. Secure your physical card

It sounds basic, but it matters. Make sure company cards are stored safely, especially when traveling or shipping them to employees. Avoid sharing cards across teams whenever possible too, because what might feel convenient at first can quickly become a point of vulnerability.

2. Guard your credit card information

Stick to secure, trusted websites when entering payment details, and avoid public Wi-Fi for financial transactions. If you can, don’t store card numbers in retailer profiles or software tools. It’s one less place your data can be compromised.

3. Monitor your accounts

Set up alerts for every transaction, or at least those over a certain threshold. It’s one of the easiest ways to flag unexpected activity fast. Then, make account reviews part of your weekly or monthly close process, not just something you check when something seems off.

4. Stay vigilant against identity theft

Unsolicited calls, emails, or texts asking for sensitive business information should always raise a red flag. Use strong, unique passwords for all financial platforms, and enable multi-factor authentication wherever it’s available.

5. Leverage solutions like virtual credit cards for added security

Virtual cards are one of the most effective ways to reduce risk that comes with physical cards, especially in card-not-present transactions. They let you set spend limits, expiration dates, and vendor-specific usage rules, so even if card details are exposed, the damage is contained and minimal.

Virtual cards offer a simple but powerful way to reduce fraud risk, especially if you manage multiple users, vendors, and recurring payments in your business. Unlike physical cards, virtual cards are generated digitally and come with built-in controls that make them harder to misuse.

Here’s what makes them more secure:

Here are a couple of common ways you can use virtual cards in your business:

Even with the right safeguards in place, fraud can still happen. The key is acting quickly to limit the fallout and prevent it from happening again.

1. Contact your card issuer immediately

Report any suspicious activity and ask them to freeze or close the compromised card. Many issuers can reissue a new number on the spot and help reverse unauthorized charges. The faster you act, the less damage fraudsters can do.

2. Notify the credit bureaus

Place a fraud alert with the major credit bureaus—Experian, Equifax, and TransUnion. This flags your business credit profile and adds an extra layer of verification if someone tries to open a new account using your information.

3. Report the fraud to the FTC

You can file a report with the Federal Trade Commission. If the fraud involves a data breach, phishing scam, or impersonation attempt, this helps build a paper trail and supports broader investigations.

4. File a police report if needed

For large losses or clear cases of identity theft, you may also want to contact local law enforcement. This is especially important if a vendor or internal party is involved.

5. Take steps to prevent it from happening again

Spend & expense management tools that allow you to create virtual credit cards can help you build better controls going forward. By using virtual cards instead of traditional cards, it’ll be much easier to avoid the risk that comes with card sharing.

In my experience, the best protection isn’t reactive, it’s embedded into the tools teams use every day. That’s where Extend stands out for safer spend and expense management.

Even better: Extend works with the business credit card you already have. No need to switch banks or disrupt reward programs to get started, just more security and fewer manual steps.

Moral of the story: Fraud doesn’t just impact your bottom line, it disrupts your team, your operations, and your peace of mind. The more you understand how it works, the better prepared you’ll be to stop it before it spreads.

With the right habits and tools, you can protect your business and keep spending secure.

Credit cards keep business moving—until someone else starts using them without permission.

Whether it’s a stolen card, a hacked account, or charges you never authorized, credit card fraud is more common than most people think and more disruptive than you might expect. It affects businesses of all sizes, with consequences that range from lost revenue to broken trust with customers, vendors, and partners.

Even the most organized teams can get blindsided. And it’s because fraud often starts quietly. A strange charge here. A flagged transaction there. But those small warning signs can snowball fast, creating bigger financial and operational headaches if they go unchecked.

And it’s only becoming more common. In 2024 alone, 62 million Americans experienced some form of credit card fraud, totaling more than $6.2 billion in unauthorized purchases.

It’s truly not a matter of if you’ll be impacted, but when.

In this blog post, I’ll share what to watch out for, how to stay ahead of potential fraud, and the modern business tools that can help make prevention easier and a lot more effective.

Credit card fraud can take many forms, but most cases fall into a handful of well-known tactics. Knowing what these look like is the first step toward spotting and stopping them early.

1. Physical card theft

This is the most straightforward type of fraud: someone gets hold of the actual credit card and uses it to make unauthorized purchases. It can happen through a lost or stolen wallet, sharing credit cards among teams, or even cards intercepted in the mail.

2. Card-not-present fraud

In this case, the thief doesn’t need the physical card, just the numbers. Online and phone transactions are especially vulnerable, since they rely on sharing the card details. If the card number is compromised in a data breach or phishing attack, it can be used in these scenarios without ever having to touch the card itself.

3. Account takeover

Here, fraudsters gain access to the company’s credit card account by manipulating personal or business information, like login credentials, billing addresses, or even employee details. Once inside, they can change passwords and account settings, reroute cards, or quietly rack up charges under your business’s name.

4. Application fraud

This type of fraud involves someone using stolen business details, like tax IDs, addresses, or employee information, to open entirely new credit card accounts. It’s especially dangerous because it can go undetected until bills show up or credit limits are maxed out.

5. Cloning and skimming

If employees use cards at gas stations, ATMs, or point-of-sale systems, they could encounter card skimmers, which are small devices that capture magnetic stripe data. That data can then be cloned and used to make fraudulent purchases elsewhere, often before anyone notices.

6. Data breaches

Sometimes the risk isn’t internal. A vendor, platform, or payment processor your business works with might go through a breach, exposing your company’s card numbers or associated employee info. These breaches often feed larger fraud schemes, especially in card-not-present scenarios.

Each method looks a bit different, but the end result is the same: unauthorized access to your credit card account, often without you even realizing it until the damage is done.

You’re likely thinking about the money lost when credit card fraud hits. But the real cost goes far beyond a few unauthorized charges.

Even if you catch the fraud and get reimbursed, there’s often a lag that can create real problems. You may end up covering lost inventory, paying higher interest, or dealing with issuer fees. And let’s not forget chargebacks, which hit hard when you’re already working to manage cash flow.

Fraud doesn’t just drain money, but time. The minute something suspicious happens, you’re pulling in finance, operations, maybe even IT. Teams lose access to cards, vendor payments get held up, and someone has to piece it all back together. That’s time that could’ve been spent on higher-value work.

Trust matters. A missed payment, or even the impression that your systems aren’t secure, can put vendor relationships at risk or stall important projects. It introduces friction at a time when you need things to run smoothly.

There’s a mental load, too. Investigating fraud, reissuing cards, updating payment methods across platforms and vendors—it all adds up. For lean finance teams, it’s a heavy lift on top of everything else they’re already juggling.

The earlier you catch fraud, the easier it’ll be to contain the damage. Here are a few warning signs that something might be off:

Manual reviews aren’t enough. To catch issues early, businesses need to layer in tools that offer real-time visibility:

Building these habits into your monthly rhythm can make fraud detection feel less like a scramble and more like part of the process.

Follow these five practical steps to prevent fraud:

1. Secure your physical card

It sounds basic, but it matters. Make sure company cards are stored safely, especially when traveling or shipping them to employees. Avoid sharing cards across teams whenever possible too, because what might feel convenient at first can quickly become a point of vulnerability.

2. Guard your credit card information

Stick to secure, trusted websites when entering payment details, and avoid public Wi-Fi for financial transactions. If you can, don’t store card numbers in retailer profiles or software tools. It’s one less place your data can be compromised.

3. Monitor your accounts

Set up alerts for every transaction, or at least those over a certain threshold. It’s one of the easiest ways to flag unexpected activity fast. Then, make account reviews part of your weekly or monthly close process, not just something you check when something seems off.

4. Stay vigilant against identity theft

Unsolicited calls, emails, or texts asking for sensitive business information should always raise a red flag. Use strong, unique passwords for all financial platforms, and enable multi-factor authentication wherever it’s available.

5. Leverage solutions like virtual credit cards for added security

Virtual cards are one of the most effective ways to reduce risk that comes with physical cards, especially in card-not-present transactions. They let you set spend limits, expiration dates, and vendor-specific usage rules, so even if card details are exposed, the damage is contained and minimal.

Virtual cards offer a simple but powerful way to reduce fraud risk, especially if you manage multiple users, vendors, and recurring payments in your business. Unlike physical cards, virtual cards are generated digitally and come with built-in controls that make them harder to misuse.

Here’s what makes them more secure:

Here are a couple of common ways you can use virtual cards in your business:

Even with the right safeguards in place, fraud can still happen. The key is acting quickly to limit the fallout and prevent it from happening again.

1. Contact your card issuer immediately

Report any suspicious activity and ask them to freeze or close the compromised card. Many issuers can reissue a new number on the spot and help reverse unauthorized charges. The faster you act, the less damage fraudsters can do.

2. Notify the credit bureaus

Place a fraud alert with the major credit bureaus—Experian, Equifax, and TransUnion. This flags your business credit profile and adds an extra layer of verification if someone tries to open a new account using your information.

3. Report the fraud to the FTC

You can file a report with the Federal Trade Commission. If the fraud involves a data breach, phishing scam, or impersonation attempt, this helps build a paper trail and supports broader investigations.

4. File a police report if needed

For large losses or clear cases of identity theft, you may also want to contact local law enforcement. This is especially important if a vendor or internal party is involved.

5. Take steps to prevent it from happening again

Spend & expense management tools that allow you to create virtual credit cards can help you build better controls going forward. By using virtual cards instead of traditional cards, it’ll be much easier to avoid the risk that comes with card sharing.

In my experience, the best protection isn’t reactive, it’s embedded into the tools teams use every day. That’s where Extend stands out for safer spend and expense management.

Even better: Extend works with the business credit card you already have. No need to switch banks or disrupt reward programs to get started, just more security and fewer manual steps.

Moral of the story: Fraud doesn’t just impact your bottom line, it disrupts your team, your operations, and your peace of mind. The more you understand how it works, the better prepared you’ll be to stop it before it spreads.

With the right habits and tools, you can protect your business and keep spending secure.

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)