Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

June 17, 2026 8:00 PM

Most finance teams already have informal rules about payment methods. Software subscriptions go on the corporate card. Large vendor invoices go via ACH or wire. Petty cash needs get reimbursed at month-end. These habits make sense individually — but when they're never formalized, they become the source of some of finance's most persistent headaches: duplicate charges no one caught, a vendor paid by wire when a card would have earned rewards, or a recurring subscription that kept charging a departed employee's card.

The reality is that payment method selection is a control decision, not just a logistical one. The method you choose determines what you can see, what you can limit, and how quickly you can close your books. Finance teams that treat this decision deliberately — rather than reactively — end up with cleaner data, fewer surprises, and significantly less manual cleanup at month-end.

Every payment method comes with a different set of tradeoffs. Checks give you a paper trail, but they're slow, manual, and offer no built-in controls against overpayment. Wire transfers are fast and final, but reversing one — if you catch an error — is a process in itself. ACH is cost-effective for high-value vendor payments, but offers minimal visibility between initiation and settlement. Corporate credit cards are flexible and earn rewards, but a single shared card number can quickly become an audit problem when multiple people have access to it.

Virtual cards sit at the far end of the control spectrum. Because each card can be issued with a specific spend limit, expiration date, and merchant restriction, they turn the payment instrument itself into a control mechanism. Your finance team isn't just choosing how to pay — they're defining exactly what that payment can and can't do before it ever hits a vendor's terminal.

This matters more than most finance leaders realize. When your payment method inherently enforces the rules you've already set, you spend less time reviewing charges after the fact and more time on the analysis that actually moves the business forward.

For a deeper look at how Extend's virtual card features work in practice, the platform overview is a good starting point.

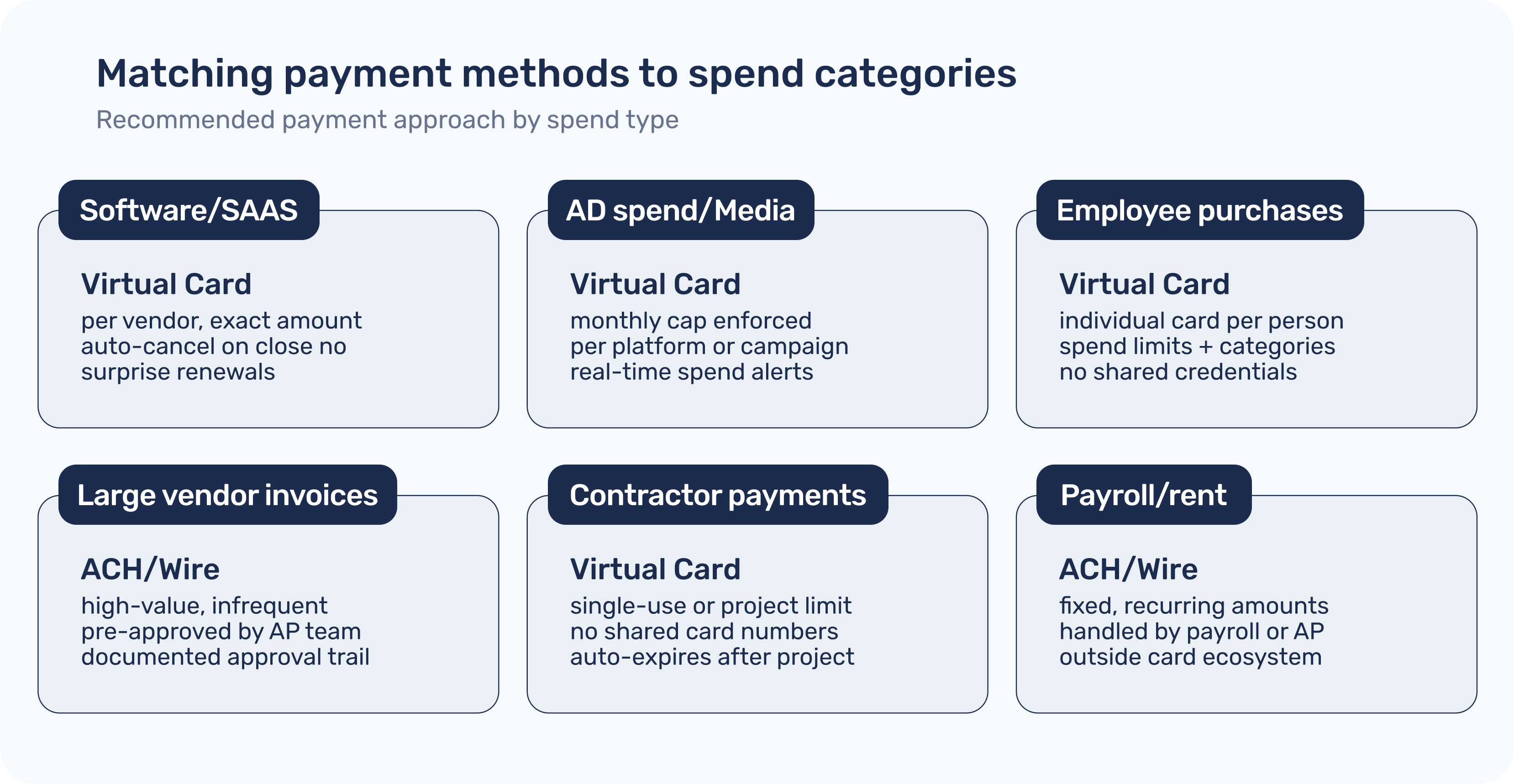

Not all spend is equal, and not all spend categories need the same level of control. Payroll goes through payroll software. Rent is a wire or a check. But several categories are consistently underserved by traditional payment methods — and those are exactly where virtual cards make the biggest difference:

- Software subscriptions and SaaS vendors. Most software vendors charge monthly or annually. When a subscription renews on a shared card, it's easy to miss — especially if the person who set it up has left the company. Virtual cards issued per vendor, with the exact subscription amount as the spend limit, eliminate accidental renewals and make cancellation as simple as closing the card.

- Ad spend and media buys. Digital advertising platforms can rack up charges quickly and unpredictably. Issuing a virtual card with a monthly budget cap tied to your media team's allocation means your finance team stays in control even when campaigns are running 24/7.

- Contractor and freelancer payments. One-time or project-based vendors often receive access to shared card credentials, which is a compliance and security risk. A per-project virtual card with a defined limit closes that window immediately.

- Employee purchasing. As our recent post on giving employees spending flexibility without losing financial control covers, the alternative to shared card numbers is individual virtual cards with per-employee budgets. Employees get the autonomy they need; finance gets the controls they need.

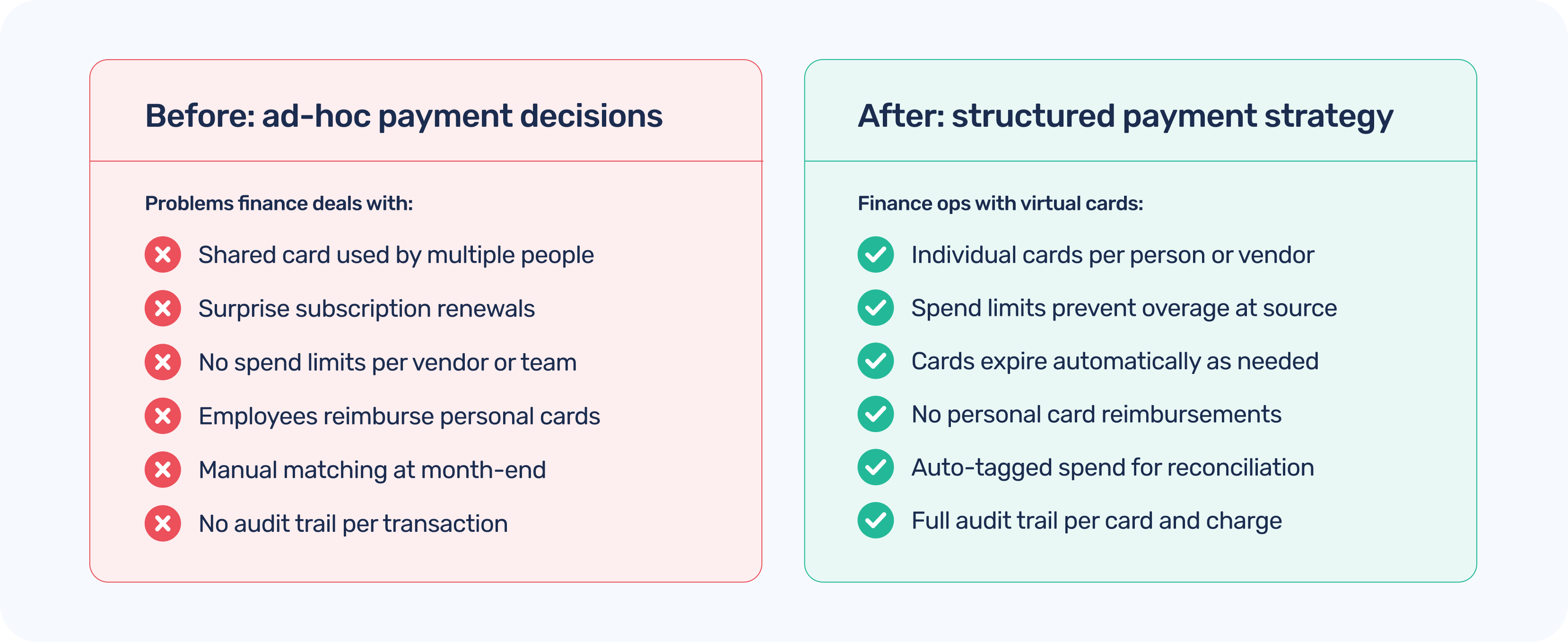

The most common failure mode for payment strategies isn't design — it's enforcement. A policy document that requires employees to request a purchase order before using the corporate card is only as good as the friction it takes to bypass it. When the alternative is 'just put it on my personal card and expense it,' many employees will choose the path of least resistance.

Effective payment policies make the right choice the easiest choice. That means building structure into the payment instrument itself, not just into a PDF policy guide. When every employee has their own virtual card with a defined budget and spend categories already set, there's nothing to bypass — the card simply won't authorize a charge that falls outside the policy. The biggest leakage points in business spending are almost always the moments where a structured process doesn't exist.

A practical payment strategy document should answer four questions for every spend category:

1. What's the preferred payment method?

2. Who has authorization to initiate it?

3. What's the approval threshold?

4. Who reconciles it at month-end?

Extend's budget management and spend control features are designed to operationalize exactly those four questions — without requiring a complex software rollout or a switch from your existing bank.

The month-end close is where sloppy payment habits show up as real cost. Every transaction that uses the wrong payment method, the wrong card, or no defined category is a transaction someone on your team has to track down, categorize, and manually match against a statement or invoice. Over a month with dozens or hundreds of transactions, that adds up to hours of work — and a close process that consistently runs longer than it should.

When payment method decisions are made proactively — with virtual cards for controllable spend, ACH for large vendor invoices, and a documented policy for the rest — the reconciliation data is largely structured before the month even ends. Transactions are already tagged to the right department, vendor, or budget. Receipts can be attached in real time via Extend's receipt management tools. And through your accounting integration, whether it's with QuickBooks, NetSuite, Microsoft 365 Dynamics, Xero, or Sage Intacct, you can pick up clean, pre-categorized data rather than a raw feed that requires manual interpretation.

Finance teams that match payment methods to spend categories — using virtual cards for controllable, recurring, or vendor-specific spend — report faster closes, fewer unauthorized charges, and significantly less time spent on manual reconciliation.

The lever isn't complicated: when the payment instrument itself enforces the rules, finance stops being a cleanup crew and starts being a strategic function. Individual virtual cards per employee or vendor eliminate the shared-card problem. Per-card spend limits enforce budgets proactively. Auto-expiring cards close the door on forgotten subscriptions. And real-time transaction data means the data your team needs for close is ready before the month ends, not two weeks after it does.

Building a smarter payment strategy doesn't require a major systems overhaul. It starts with a clear map of your spend categories and a decision about which payment method best fits each one. For most finance teams, that analysis quickly reveals that virtual cards are underused — especially for the types of spend that cause the most reconciliation pain.

Extend gives finance teams the tools to act on that insight immediately: virtual cards built on top of your existing business credit card, with budgets, spend controls, receipt capture, and accounting integrations that work together as a unified system. Whether your team manages employee purchasing, vendor payments, ad spend, or contractor relationships, the workflow is the same — issue a card with the right parameters, assign it to the right person or vendor, and let the controls do their job.

If your team is ready to formalize your payment strategy, start with a look at how vendor payment management works in Extend, or explore how expense management connects across the full spend lifecycle.

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Most finance teams already have informal rules about payment methods. Software subscriptions go on the corporate card. Large vendor invoices go via ACH or wire. Petty cash needs get reimbursed at month-end. These habits make sense individually — but when they're never formalized, they become the source of some of finance's most persistent headaches: duplicate charges no one caught, a vendor paid by wire when a card would have earned rewards, or a recurring subscription that kept charging a departed employee's card.

The reality is that payment method selection is a control decision, not just a logistical one. The method you choose determines what you can see, what you can limit, and how quickly you can close your books. Finance teams that treat this decision deliberately — rather than reactively — end up with cleaner data, fewer surprises, and significantly less manual cleanup at month-end.

Every payment method comes with a different set of tradeoffs. Checks give you a paper trail, but they're slow, manual, and offer no built-in controls against overpayment. Wire transfers are fast and final, but reversing one — if you catch an error — is a process in itself. ACH is cost-effective for high-value vendor payments, but offers minimal visibility between initiation and settlement. Corporate credit cards are flexible and earn rewards, but a single shared card number can quickly become an audit problem when multiple people have access to it.

Virtual cards sit at the far end of the control spectrum. Because each card can be issued with a specific spend limit, expiration date, and merchant restriction, they turn the payment instrument itself into a control mechanism. Your finance team isn't just choosing how to pay — they're defining exactly what that payment can and can't do before it ever hits a vendor's terminal.

This matters more than most finance leaders realize. When your payment method inherently enforces the rules you've already set, you spend less time reviewing charges after the fact and more time on the analysis that actually moves the business forward.

For a deeper look at how Extend's virtual card features work in practice, the platform overview is a good starting point.

Not all spend is equal, and not all spend categories need the same level of control. Payroll goes through payroll software. Rent is a wire or a check. But several categories are consistently underserved by traditional payment methods — and those are exactly where virtual cards make the biggest difference:

- Software subscriptions and SaaS vendors. Most software vendors charge monthly or annually. When a subscription renews on a shared card, it's easy to miss — especially if the person who set it up has left the company. Virtual cards issued per vendor, with the exact subscription amount as the spend limit, eliminate accidental renewals and make cancellation as simple as closing the card.

- Ad spend and media buys. Digital advertising platforms can rack up charges quickly and unpredictably. Issuing a virtual card with a monthly budget cap tied to your media team's allocation means your finance team stays in control even when campaigns are running 24/7.

- Contractor and freelancer payments. One-time or project-based vendors often receive access to shared card credentials, which is a compliance and security risk. A per-project virtual card with a defined limit closes that window immediately.

- Employee purchasing. As our recent post on giving employees spending flexibility without losing financial control covers, the alternative to shared card numbers is individual virtual cards with per-employee budgets. Employees get the autonomy they need; finance gets the controls they need.

The most common failure mode for payment strategies isn't design — it's enforcement. A policy document that requires employees to request a purchase order before using the corporate card is only as good as the friction it takes to bypass it. When the alternative is 'just put it on my personal card and expense it,' many employees will choose the path of least resistance.

Effective payment policies make the right choice the easiest choice. That means building structure into the payment instrument itself, not just into a PDF policy guide. When every employee has their own virtual card with a defined budget and spend categories already set, there's nothing to bypass — the card simply won't authorize a charge that falls outside the policy. The biggest leakage points in business spending are almost always the moments where a structured process doesn't exist.

A practical payment strategy document should answer four questions for every spend category:

1. What's the preferred payment method?

2. Who has authorization to initiate it?

3. What's the approval threshold?

4. Who reconciles it at month-end?

Extend's budget management and spend control features are designed to operationalize exactly those four questions — without requiring a complex software rollout or a switch from your existing bank.

The month-end close is where sloppy payment habits show up as real cost. Every transaction that uses the wrong payment method, the wrong card, or no defined category is a transaction someone on your team has to track down, categorize, and manually match against a statement or invoice. Over a month with dozens or hundreds of transactions, that adds up to hours of work — and a close process that consistently runs longer than it should.

When payment method decisions are made proactively — with virtual cards for controllable spend, ACH for large vendor invoices, and a documented policy for the rest — the reconciliation data is largely structured before the month even ends. Transactions are already tagged to the right department, vendor, or budget. Receipts can be attached in real time via Extend's receipt management tools. And through your accounting integration, whether it's with QuickBooks, NetSuite, Microsoft 365 Dynamics, Xero, or Sage Intacct, you can pick up clean, pre-categorized data rather than a raw feed that requires manual interpretation.

Finance teams that match payment methods to spend categories — using virtual cards for controllable, recurring, or vendor-specific spend — report faster closes, fewer unauthorized charges, and significantly less time spent on manual reconciliation.

The lever isn't complicated: when the payment instrument itself enforces the rules, finance stops being a cleanup crew and starts being a strategic function. Individual virtual cards per employee or vendor eliminate the shared-card problem. Per-card spend limits enforce budgets proactively. Auto-expiring cards close the door on forgotten subscriptions. And real-time transaction data means the data your team needs for close is ready before the month ends, not two weeks after it does.

Building a smarter payment strategy doesn't require a major systems overhaul. It starts with a clear map of your spend categories and a decision about which payment method best fits each one. For most finance teams, that analysis quickly reveals that virtual cards are underused — especially for the types of spend that cause the most reconciliation pain.

Extend gives finance teams the tools to act on that insight immediately: virtual cards built on top of your existing business credit card, with budgets, spend controls, receipt capture, and accounting integrations that work together as a unified system. Whether your team manages employee purchasing, vendor payments, ad spend, or contractor relationships, the workflow is the same — issue a card with the right parameters, assign it to the right person or vendor, and let the controls do their job.

If your team is ready to formalize your payment strategy, start with a look at how vendor payment management works in Extend, or explore how expense management connects across the full spend lifecycle.

Most finance teams already have informal rules about payment methods. Software subscriptions go on the corporate card. Large vendor invoices go via ACH or wire. Petty cash needs get reimbursed at month-end. These habits make sense individually — but when they're never formalized, they become the source of some of finance's most persistent headaches: duplicate charges no one caught, a vendor paid by wire when a card would have earned rewards, or a recurring subscription that kept charging a departed employee's card.

The reality is that payment method selection is a control decision, not just a logistical one. The method you choose determines what you can see, what you can limit, and how quickly you can close your books. Finance teams that treat this decision deliberately — rather than reactively — end up with cleaner data, fewer surprises, and significantly less manual cleanup at month-end.

Every payment method comes with a different set of tradeoffs. Checks give you a paper trail, but they're slow, manual, and offer no built-in controls against overpayment. Wire transfers are fast and final, but reversing one — if you catch an error — is a process in itself. ACH is cost-effective for high-value vendor payments, but offers minimal visibility between initiation and settlement. Corporate credit cards are flexible and earn rewards, but a single shared card number can quickly become an audit problem when multiple people have access to it.

Virtual cards sit at the far end of the control spectrum. Because each card can be issued with a specific spend limit, expiration date, and merchant restriction, they turn the payment instrument itself into a control mechanism. Your finance team isn't just choosing how to pay — they're defining exactly what that payment can and can't do before it ever hits a vendor's terminal.

This matters more than most finance leaders realize. When your payment method inherently enforces the rules you've already set, you spend less time reviewing charges after the fact and more time on the analysis that actually moves the business forward.

For a deeper look at how Extend's virtual card features work in practice, the platform overview is a good starting point.

Not all spend is equal, and not all spend categories need the same level of control. Payroll goes through payroll software. Rent is a wire or a check. But several categories are consistently underserved by traditional payment methods — and those are exactly where virtual cards make the biggest difference:

- Software subscriptions and SaaS vendors. Most software vendors charge monthly or annually. When a subscription renews on a shared card, it's easy to miss — especially if the person who set it up has left the company. Virtual cards issued per vendor, with the exact subscription amount as the spend limit, eliminate accidental renewals and make cancellation as simple as closing the card.

- Ad spend and media buys. Digital advertising platforms can rack up charges quickly and unpredictably. Issuing a virtual card with a monthly budget cap tied to your media team's allocation means your finance team stays in control even when campaigns are running 24/7.

- Contractor and freelancer payments. One-time or project-based vendors often receive access to shared card credentials, which is a compliance and security risk. A per-project virtual card with a defined limit closes that window immediately.

- Employee purchasing. As our recent post on giving employees spending flexibility without losing financial control covers, the alternative to shared card numbers is individual virtual cards with per-employee budgets. Employees get the autonomy they need; finance gets the controls they need.

The most common failure mode for payment strategies isn't design — it's enforcement. A policy document that requires employees to request a purchase order before using the corporate card is only as good as the friction it takes to bypass it. When the alternative is 'just put it on my personal card and expense it,' many employees will choose the path of least resistance.

Effective payment policies make the right choice the easiest choice. That means building structure into the payment instrument itself, not just into a PDF policy guide. When every employee has their own virtual card with a defined budget and spend categories already set, there's nothing to bypass — the card simply won't authorize a charge that falls outside the policy. The biggest leakage points in business spending are almost always the moments where a structured process doesn't exist.

A practical payment strategy document should answer four questions for every spend category:

1. What's the preferred payment method?

2. Who has authorization to initiate it?

3. What's the approval threshold?

4. Who reconciles it at month-end?

Extend's budget management and spend control features are designed to operationalize exactly those four questions — without requiring a complex software rollout or a switch from your existing bank.

The month-end close is where sloppy payment habits show up as real cost. Every transaction that uses the wrong payment method, the wrong card, or no defined category is a transaction someone on your team has to track down, categorize, and manually match against a statement or invoice. Over a month with dozens or hundreds of transactions, that adds up to hours of work — and a close process that consistently runs longer than it should.

When payment method decisions are made proactively — with virtual cards for controllable spend, ACH for large vendor invoices, and a documented policy for the rest — the reconciliation data is largely structured before the month even ends. Transactions are already tagged to the right department, vendor, or budget. Receipts can be attached in real time via Extend's receipt management tools. And through your accounting integration, whether it's with QuickBooks, NetSuite, Microsoft 365 Dynamics, Xero, or Sage Intacct, you can pick up clean, pre-categorized data rather than a raw feed that requires manual interpretation.

Finance teams that match payment methods to spend categories — using virtual cards for controllable, recurring, or vendor-specific spend — report faster closes, fewer unauthorized charges, and significantly less time spent on manual reconciliation.

The lever isn't complicated: when the payment instrument itself enforces the rules, finance stops being a cleanup crew and starts being a strategic function. Individual virtual cards per employee or vendor eliminate the shared-card problem. Per-card spend limits enforce budgets proactively. Auto-expiring cards close the door on forgotten subscriptions. And real-time transaction data means the data your team needs for close is ready before the month ends, not two weeks after it does.

Building a smarter payment strategy doesn't require a major systems overhaul. It starts with a clear map of your spend categories and a decision about which payment method best fits each one. For most finance teams, that analysis quickly reveals that virtual cards are underused — especially for the types of spend that cause the most reconciliation pain.

Extend gives finance teams the tools to act on that insight immediately: virtual cards built on top of your existing business credit card, with budgets, spend controls, receipt capture, and accounting integrations that work together as a unified system. Whether your team manages employee purchasing, vendor payments, ad spend, or contractor relationships, the workflow is the same — issue a card with the right parameters, assign it to the right person or vendor, and let the controls do their job.

If your team is ready to formalize your payment strategy, start with a look at how vendor payment management works in Extend, or explore how expense management connects across the full spend lifecycle.

Most finance teams already have informal rules about payment methods. Software subscriptions go on the corporate card. Large vendor invoices go via ACH or wire. Petty cash needs get reimbursed at month-end. These habits make sense individually — but when they're never formalized, they become the source of some of finance's most persistent headaches: duplicate charges no one caught, a vendor paid by wire when a card would have earned rewards, or a recurring subscription that kept charging a departed employee's card.

The reality is that payment method selection is a control decision, not just a logistical one. The method you choose determines what you can see, what you can limit, and how quickly you can close your books. Finance teams that treat this decision deliberately — rather than reactively — end up with cleaner data, fewer surprises, and significantly less manual cleanup at month-end.

Every payment method comes with a different set of tradeoffs. Checks give you a paper trail, but they're slow, manual, and offer no built-in controls against overpayment. Wire transfers are fast and final, but reversing one — if you catch an error — is a process in itself. ACH is cost-effective for high-value vendor payments, but offers minimal visibility between initiation and settlement. Corporate credit cards are flexible and earn rewards, but a single shared card number can quickly become an audit problem when multiple people have access to it.

Virtual cards sit at the far end of the control spectrum. Because each card can be issued with a specific spend limit, expiration date, and merchant restriction, they turn the payment instrument itself into a control mechanism. Your finance team isn't just choosing how to pay — they're defining exactly what that payment can and can't do before it ever hits a vendor's terminal.

This matters more than most finance leaders realize. When your payment method inherently enforces the rules you've already set, you spend less time reviewing charges after the fact and more time on the analysis that actually moves the business forward.

For a deeper look at how Extend's virtual card features work in practice, the platform overview is a good starting point.

Not all spend is equal, and not all spend categories need the same level of control. Payroll goes through payroll software. Rent is a wire or a check. But several categories are consistently underserved by traditional payment methods — and those are exactly where virtual cards make the biggest difference:

- Software subscriptions and SaaS vendors. Most software vendors charge monthly or annually. When a subscription renews on a shared card, it's easy to miss — especially if the person who set it up has left the company. Virtual cards issued per vendor, with the exact subscription amount as the spend limit, eliminate accidental renewals and make cancellation as simple as closing the card.

- Ad spend and media buys. Digital advertising platforms can rack up charges quickly and unpredictably. Issuing a virtual card with a monthly budget cap tied to your media team's allocation means your finance team stays in control even when campaigns are running 24/7.

- Contractor and freelancer payments. One-time or project-based vendors often receive access to shared card credentials, which is a compliance and security risk. A per-project virtual card with a defined limit closes that window immediately.

- Employee purchasing. As our recent post on giving employees spending flexibility without losing financial control covers, the alternative to shared card numbers is individual virtual cards with per-employee budgets. Employees get the autonomy they need; finance gets the controls they need.

The most common failure mode for payment strategies isn't design — it's enforcement. A policy document that requires employees to request a purchase order before using the corporate card is only as good as the friction it takes to bypass it. When the alternative is 'just put it on my personal card and expense it,' many employees will choose the path of least resistance.

Effective payment policies make the right choice the easiest choice. That means building structure into the payment instrument itself, not just into a PDF policy guide. When every employee has their own virtual card with a defined budget and spend categories already set, there's nothing to bypass — the card simply won't authorize a charge that falls outside the policy. The biggest leakage points in business spending are almost always the moments where a structured process doesn't exist.

A practical payment strategy document should answer four questions for every spend category:

1. What's the preferred payment method?

2. Who has authorization to initiate it?

3. What's the approval threshold?

4. Who reconciles it at month-end?

Extend's budget management and spend control features are designed to operationalize exactly those four questions — without requiring a complex software rollout or a switch from your existing bank.

The month-end close is where sloppy payment habits show up as real cost. Every transaction that uses the wrong payment method, the wrong card, or no defined category is a transaction someone on your team has to track down, categorize, and manually match against a statement or invoice. Over a month with dozens or hundreds of transactions, that adds up to hours of work — and a close process that consistently runs longer than it should.

When payment method decisions are made proactively — with virtual cards for controllable spend, ACH for large vendor invoices, and a documented policy for the rest — the reconciliation data is largely structured before the month even ends. Transactions are already tagged to the right department, vendor, or budget. Receipts can be attached in real time via Extend's receipt management tools. And through your accounting integration, whether it's with QuickBooks, NetSuite, Microsoft 365 Dynamics, Xero, or Sage Intacct, you can pick up clean, pre-categorized data rather than a raw feed that requires manual interpretation.

Finance teams that match payment methods to spend categories — using virtual cards for controllable, recurring, or vendor-specific spend — report faster closes, fewer unauthorized charges, and significantly less time spent on manual reconciliation.

The lever isn't complicated: when the payment instrument itself enforces the rules, finance stops being a cleanup crew and starts being a strategic function. Individual virtual cards per employee or vendor eliminate the shared-card problem. Per-card spend limits enforce budgets proactively. Auto-expiring cards close the door on forgotten subscriptions. And real-time transaction data means the data your team needs for close is ready before the month ends, not two weeks after it does.

Building a smarter payment strategy doesn't require a major systems overhaul. It starts with a clear map of your spend categories and a decision about which payment method best fits each one. For most finance teams, that analysis quickly reveals that virtual cards are underused — especially for the types of spend that cause the most reconciliation pain.

Extend gives finance teams the tools to act on that insight immediately: virtual cards built on top of your existing business credit card, with budgets, spend controls, receipt capture, and accounting integrations that work together as a unified system. Whether your team manages employee purchasing, vendor payments, ad spend, or contractor relationships, the workflow is the same — issue a card with the right parameters, assign it to the right person or vendor, and let the controls do their job.

If your team is ready to formalize your payment strategy, start with a look at how vendor payment management works in Extend, or explore how expense management connects across the full spend lifecycle.

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)