Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

June 5, 2026 4:28 PM

Most finance conversations about expense documentation focus on the administrative side: getting receipts in, coding transactions correctly, and closing out expense reports on time. The tax consequences of failing to do this properly are less often discussed, but they are significant, and they affect both the company and individual employees.

Here is what actually happens when business expenses cannot be properly substantiated.

When a company reimburses employees for business expenses, the tax treatment of those reimbursements depends on whether the company operates an "accountable plan" as defined by IRS regulations. An accountable plan has three requirements: the expense must have a business connection, the employee must substantiate the expense with adequate documentation, and any excess reimbursement must be returned to the employer within a reasonable time.

When these conditions are met, reimbursements are excluded from the employee's taxable income, and the company gets the deduction. When any one of these conditions is not met, the reimbursement is treated as wages, subject to income tax withholding, FICA, and reporting on the employee's W-2.

Three conditions must all be met:

1. The expense must have a legitimate business purpose

2. The employee must provide adequate documentation within a reasonable time

3. Any excess reimbursement above the documented amount must be returned.

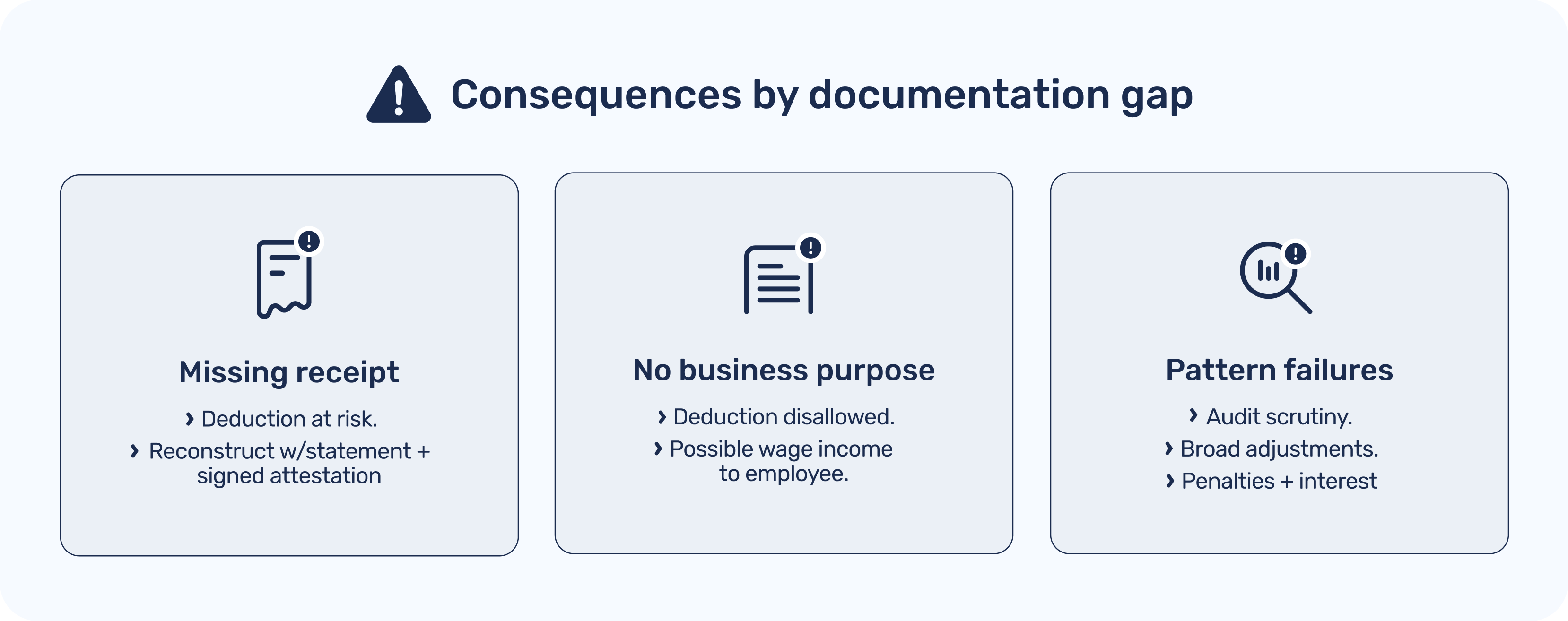

The most common outcome of inadequate expense documentation is the disallowance of the deduction in an audit. The IRS examiner asks for receipts and business purpose records. Finance cannot produce them. The deduction is denied, the taxable income goes up, and penalties and interest are assessed on the underpayment.

For travel and entertainment expenses, the standard is particularly demanding. Section 274 of the tax code requires documentation of the amount, date, location, business purpose, and business relationship to each person involved. A credit card statement showing a restaurant charge is not sufficient. The original itemized receipt, plus a record of who attended and what was discussed, is required.

In audits, the IRS looks for patterns. A handful of missing receipts in a large expense program is typically handled through negotiation and partial disallowance. A consistent pattern of inadequate documentation across a category, client entertainment, for example, raises questions about whether those expenses were genuinely business-related and can result in broader adjustments.

This is the part that often surprises people: when an expense reimbursement fails the accountable plan test, the liability does not stay with the company. It moves to the employee. A reimbursement that should have been excluded from income becomes taxable wages. The employee owes income tax on it. The company owes payroll taxes. And if this was not withheld correctly, there may be penalties on both sides.

For employees who received substantial reimbursements in a year where documentation was inadequate, the adjustment on audit can be significant. This is why CFOs and controllers at companies with active T&E programs take documentation requirements seriously, not just for the corporate deduction, but because the alternative is employee tax liability that creates legal and HR problems on top of the tax problem.

The practical defense against substantiation problems is not a better policy document. It is documentation capture that happens automatically at the point of purchase, before the context is lost and before the administrative burden of retroactive collection sets in.

Virtual cards create natural checkpoints for this. When a charge posts to a purpose-specific virtual card, the cardholder gets an immediate notification with a prompt to add the receipt and memo. The business purpose is often already captured in the card's configuration. Finance does not have to chase documentation later because the collection happened in real time.

Extend can help you start doing this today!

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. Tax rules vary by jurisdiction and individual circumstance. Consult a qualified tax professional for guidance specific to your situation.

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Most finance conversations about expense documentation focus on the administrative side: getting receipts in, coding transactions correctly, and closing out expense reports on time. The tax consequences of failing to do this properly are less often discussed, but they are significant, and they affect both the company and individual employees.

Here is what actually happens when business expenses cannot be properly substantiated.

When a company reimburses employees for business expenses, the tax treatment of those reimbursements depends on whether the company operates an "accountable plan" as defined by IRS regulations. An accountable plan has three requirements: the expense must have a business connection, the employee must substantiate the expense with adequate documentation, and any excess reimbursement must be returned to the employer within a reasonable time.

When these conditions are met, reimbursements are excluded from the employee's taxable income, and the company gets the deduction. When any one of these conditions is not met, the reimbursement is treated as wages, subject to income tax withholding, FICA, and reporting on the employee's W-2.

Three conditions must all be met:

1. The expense must have a legitimate business purpose

2. The employee must provide adequate documentation within a reasonable time

3. Any excess reimbursement above the documented amount must be returned.

The most common outcome of inadequate expense documentation is the disallowance of the deduction in an audit. The IRS examiner asks for receipts and business purpose records. Finance cannot produce them. The deduction is denied, the taxable income goes up, and penalties and interest are assessed on the underpayment.

For travel and entertainment expenses, the standard is particularly demanding. Section 274 of the tax code requires documentation of the amount, date, location, business purpose, and business relationship to each person involved. A credit card statement showing a restaurant charge is not sufficient. The original itemized receipt, plus a record of who attended and what was discussed, is required.

In audits, the IRS looks for patterns. A handful of missing receipts in a large expense program is typically handled through negotiation and partial disallowance. A consistent pattern of inadequate documentation across a category, client entertainment, for example, raises questions about whether those expenses were genuinely business-related and can result in broader adjustments.

This is the part that often surprises people: when an expense reimbursement fails the accountable plan test, the liability does not stay with the company. It moves to the employee. A reimbursement that should have been excluded from income becomes taxable wages. The employee owes income tax on it. The company owes payroll taxes. And if this was not withheld correctly, there may be penalties on both sides.

For employees who received substantial reimbursements in a year where documentation was inadequate, the adjustment on audit can be significant. This is why CFOs and controllers at companies with active T&E programs take documentation requirements seriously, not just for the corporate deduction, but because the alternative is employee tax liability that creates legal and HR problems on top of the tax problem.

The practical defense against substantiation problems is not a better policy document. It is documentation capture that happens automatically at the point of purchase, before the context is lost and before the administrative burden of retroactive collection sets in.

Virtual cards create natural checkpoints for this. When a charge posts to a purpose-specific virtual card, the cardholder gets an immediate notification with a prompt to add the receipt and memo. The business purpose is often already captured in the card's configuration. Finance does not have to chase documentation later because the collection happened in real time.

Extend can help you start doing this today!

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. Tax rules vary by jurisdiction and individual circumstance. Consult a qualified tax professional for guidance specific to your situation.

Most finance conversations about expense documentation focus on the administrative side: getting receipts in, coding transactions correctly, and closing out expense reports on time. The tax consequences of failing to do this properly are less often discussed, but they are significant, and they affect both the company and individual employees.

Here is what actually happens when business expenses cannot be properly substantiated.

When a company reimburses employees for business expenses, the tax treatment of those reimbursements depends on whether the company operates an "accountable plan" as defined by IRS regulations. An accountable plan has three requirements: the expense must have a business connection, the employee must substantiate the expense with adequate documentation, and any excess reimbursement must be returned to the employer within a reasonable time.

When these conditions are met, reimbursements are excluded from the employee's taxable income, and the company gets the deduction. When any one of these conditions is not met, the reimbursement is treated as wages, subject to income tax withholding, FICA, and reporting on the employee's W-2.

Three conditions must all be met:

1. The expense must have a legitimate business purpose

2. The employee must provide adequate documentation within a reasonable time

3. Any excess reimbursement above the documented amount must be returned.

The most common outcome of inadequate expense documentation is the disallowance of the deduction in an audit. The IRS examiner asks for receipts and business purpose records. Finance cannot produce them. The deduction is denied, the taxable income goes up, and penalties and interest are assessed on the underpayment.

For travel and entertainment expenses, the standard is particularly demanding. Section 274 of the tax code requires documentation of the amount, date, location, business purpose, and business relationship to each person involved. A credit card statement showing a restaurant charge is not sufficient. The original itemized receipt, plus a record of who attended and what was discussed, is required.

In audits, the IRS looks for patterns. A handful of missing receipts in a large expense program is typically handled through negotiation and partial disallowance. A consistent pattern of inadequate documentation across a category, client entertainment, for example, raises questions about whether those expenses were genuinely business-related and can result in broader adjustments.

This is the part that often surprises people: when an expense reimbursement fails the accountable plan test, the liability does not stay with the company. It moves to the employee. A reimbursement that should have been excluded from income becomes taxable wages. The employee owes income tax on it. The company owes payroll taxes. And if this was not withheld correctly, there may be penalties on both sides.

For employees who received substantial reimbursements in a year where documentation was inadequate, the adjustment on audit can be significant. This is why CFOs and controllers at companies with active T&E programs take documentation requirements seriously, not just for the corporate deduction, but because the alternative is employee tax liability that creates legal and HR problems on top of the tax problem.

The practical defense against substantiation problems is not a better policy document. It is documentation capture that happens automatically at the point of purchase, before the context is lost and before the administrative burden of retroactive collection sets in.

Virtual cards create natural checkpoints for this. When a charge posts to a purpose-specific virtual card, the cardholder gets an immediate notification with a prompt to add the receipt and memo. The business purpose is often already captured in the card's configuration. Finance does not have to chase documentation later because the collection happened in real time.

Extend can help you start doing this today!

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. Tax rules vary by jurisdiction and individual circumstance. Consult a qualified tax professional for guidance specific to your situation.

Most finance conversations about expense documentation focus on the administrative side: getting receipts in, coding transactions correctly, and closing out expense reports on time. The tax consequences of failing to do this properly are less often discussed, but they are significant, and they affect both the company and individual employees.

Here is what actually happens when business expenses cannot be properly substantiated.

When a company reimburses employees for business expenses, the tax treatment of those reimbursements depends on whether the company operates an "accountable plan" as defined by IRS regulations. An accountable plan has three requirements: the expense must have a business connection, the employee must substantiate the expense with adequate documentation, and any excess reimbursement must be returned to the employer within a reasonable time.

When these conditions are met, reimbursements are excluded from the employee's taxable income, and the company gets the deduction. When any one of these conditions is not met, the reimbursement is treated as wages, subject to income tax withholding, FICA, and reporting on the employee's W-2.

Three conditions must all be met:

1. The expense must have a legitimate business purpose

2. The employee must provide adequate documentation within a reasonable time

3. Any excess reimbursement above the documented amount must be returned.

The most common outcome of inadequate expense documentation is the disallowance of the deduction in an audit. The IRS examiner asks for receipts and business purpose records. Finance cannot produce them. The deduction is denied, the taxable income goes up, and penalties and interest are assessed on the underpayment.

For travel and entertainment expenses, the standard is particularly demanding. Section 274 of the tax code requires documentation of the amount, date, location, business purpose, and business relationship to each person involved. A credit card statement showing a restaurant charge is not sufficient. The original itemized receipt, plus a record of who attended and what was discussed, is required.

In audits, the IRS looks for patterns. A handful of missing receipts in a large expense program is typically handled through negotiation and partial disallowance. A consistent pattern of inadequate documentation across a category, client entertainment, for example, raises questions about whether those expenses were genuinely business-related and can result in broader adjustments.

This is the part that often surprises people: when an expense reimbursement fails the accountable plan test, the liability does not stay with the company. It moves to the employee. A reimbursement that should have been excluded from income becomes taxable wages. The employee owes income tax on it. The company owes payroll taxes. And if this was not withheld correctly, there may be penalties on both sides.

For employees who received substantial reimbursements in a year where documentation was inadequate, the adjustment on audit can be significant. This is why CFOs and controllers at companies with active T&E programs take documentation requirements seriously, not just for the corporate deduction, but because the alternative is employee tax liability that creates legal and HR problems on top of the tax problem.

The practical defense against substantiation problems is not a better policy document. It is documentation capture that happens automatically at the point of purchase, before the context is lost and before the administrative burden of retroactive collection sets in.

Virtual cards create natural checkpoints for this. When a charge posts to a purpose-specific virtual card, the cardholder gets an immediate notification with a prompt to add the receipt and memo. The business purpose is often already captured in the card's configuration. Finance does not have to chase documentation later because the collection happened in real time.

Extend can help you start doing this today!

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. Tax rules vary by jurisdiction and individual circumstance. Consult a qualified tax professional for guidance specific to your situation.

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)