Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

June 5, 2026 4:07 PM

Every finance team has had the conversation: an employee submits an expense report weeks after a trip, the receipts are missing, and no one is quite sure whether a note on a napkin counts. It sounds like an annoyance. But the underlying issue — whether your business can substantiate its expense deductions if the IRS comes asking — is genuinely consequential.

The rules themselves are not especially complicated. The challenge is that they are easy to misremember, frequently oversimplified in casual advice, and almost never built into the moment when an employee is actually handing over a card.

Here is what the IRS actually requires, in plain language, and what finance teams can do to stay confidently prepared.

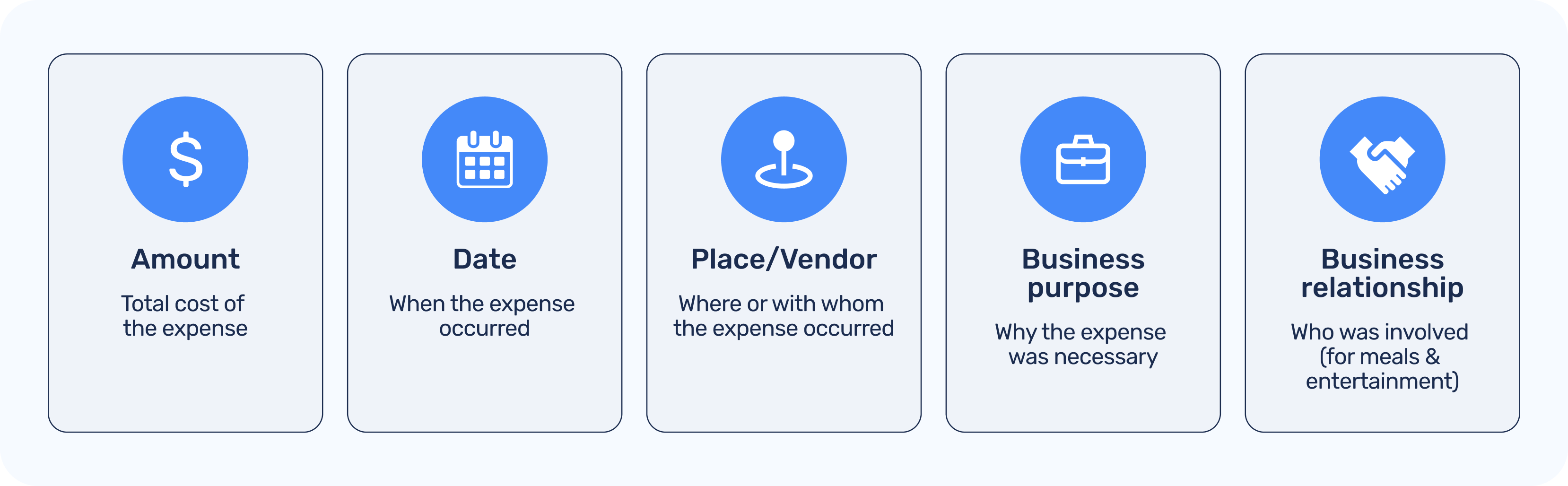

Under IRC Section 274 and the Treasury Regulations that implement it, a deductible business expense must be supported by "adequate records." The IRS defines this as documentation that establishes five distinct elements:

For most expense categories — travel, meals, lodging, supplies — a receipt from the vendor combined with a brief written note of the business purpose will satisfy all five. The receipt typically covers amount, date, and vendor. The employee's note covers the purpose and, where relevant, who was present.

The business relationship requirement comes up most often for meals and entertainment. If a client dinner is expensed, the name and business relationship of the attendees needs to be documented somewhere — whether that is a notes field in an expense report, a calendar entry, or a follow-up email.

One of the most repeated pieces of expense advice in corporate finance is "you do not need a receipt for anything under $75." It is worth unpacking what this actually means — because it is frequently overstated.

The IRS does provide simplified substantiation options for certain lower-dollar expenses. Under Revenue Procedure 98-25 and the accountable plan regulations, an employer is not required to collect documentary evidence (i.e., a receipt or invoice) for expenses under $75, provided the expense would otherwise qualify and other records are maintained. For lodging, there is no floor — receipts are always required regardless of the amount.

In practice, many finance teams choose to require receipts for all expenses, regardless of amount. This is entirely defensible from an IRS perspective and makes reconciliation significantly cleaner. The $75 threshold is a floor for required documentation, not a permission slip to stop keeping records.

The IRS confirmed in Revenue Procedure 98-25 that electronic records are acceptable, and subsequent guidance has reinforced that emailed receipts, PDF downloads, and scanned images all meet the substantiation standard — as long as the record is accurate, complete, and legible.

What matters is that the digital image or document clearly shows all five required elements. A blurry photo of a receipt where the total is unreadable does not satisfy the requirement. Neither does a partial email confirmation that shows the purchase date but omits the itemization.

The practical implication for finance teams: your receipt management workflow needs to produce complete digital records, not just proof that something was spent. This is where purpose-built tools make a real difference. For example, with a tool like Extend, employees can attach receipts directly to virtual card transactions — and because each virtual card is issued for a specific purpose or vendor, the business-purpose context is often captured before the employee even submits anything.

The general rule is that records supporting a tax return should be kept for at least three years from the date the return was filed. This covers the standard IRS audit window. However, there are circumstances that extend this obligation:

If you substantially understate income — more than 25 percent of gross income is omitted from a return — the IRS has six years to assess additional taxes. If a return is fraudulent or never filed, there is no statute of limitations. For employment tax records specifically, the IRS recommends four years from the date the tax was due or paid, whichever is later.

The practical guidance for most businesses: retain expense records and supporting receipts for at least seven years. It's longer than the standard window, but the storage cost of digital records is low, and it eliminates uncertainty in edge cases.

Beyond the basic receipt rules, three specific expense categories carry their own documentation requirements that finance teams should understand clearly.

An accountable plan is a formal employer reimbursement arrangement that meets IRS criteria: expenses must have a business connection, employees must adequately account for their expenses, and employees must return any excess reimbursement within a reasonable time. When an accountable plan is properly maintained, reimbursements are excluded from employee income and are deductible to the employer. The documentation obligations are the same five-element standard — but the plan structure itself needs to be documented in writing.

Employers who use IRS-approved per diem rates for travel and lodging can simplify documentation significantly. Instead of collecting individual meal and lodging receipts, the employer pays a daily rate, and the employee documents only the time, place, and business purpose of the travel. The per diem rates are set by the General Services Administration (GSA) and vary by location. Using per diems does not eliminate substantiation entirely — it just substitutes a standardized rate for itemized receipt collection.

For employees reimbursed for using personal vehicles, the IRS requires a contemporaneous mileage log that documents the date of the trip, the destination, the business purpose, and the number of miles driven. The standard mileage rate changes annually and is published by the IRS each December.

A few patterns come up repeatedly when businesses face scrutiny over business expense deductions:

Vague business purpose notes: "Client dinner" without the client's name, company, and the business discussed does not fully satisfy the requirement. "Dinner with Sarah Chen, CFO at Meridian Partners — discussed Q3 proposal" does. Specificity matters.

Missing vendor information on informal receipts: A cash register tape that shows only a total and date, with no vendor name or address, is insufficient on its own. A handwritten note accompanying it that adds the vendor details can fill the gap, but the better practice is to ask for a detailed receipt upfront.

Receipts that don't match the card transaction: If an employee submits a receipt for $82 and the card transaction shows $84 (perhaps because of a tip added post-receipt), the documentation needs to account for the discrepancy — usually by noting the tip separately. This is a common issue with restaurant expenses.

Retroactive reconstruction: The IRS specifically disfavors reconstructed records — documentation that was assembled after the fact rather than captured at the time of the expense. Contemporaneous records carry much more weight. This is one of the strongest arguments for capturing expense data at the point of transaction rather than at the end of the month.

Staying compliant with IRS receipt requirements is ultimately an operational challenge, not just a knowledge one. The harder part is building a system where the right documentation gets captured reliably, for every transaction, without putting the burden entirely on employees to remember the rules.

Extend is designed with this in mind.

When a virtual card is created for a specific employee, vendor, or project, the business purpose context is built in from the start. When the card is used, the transaction — including amount, date, and vendor — is recorded automatically. Employees can attach receipts directly to individual transactions via the Extend app or text and email forwarding, so the documentation lives alongside the transaction data rather than in a separate system.

For expense data beyond the basic five elements, Extend's Additional Fields for Expense Capture lets finance teams define custom fields — project codes, department tags, client names, or any other data point the business tracks — that populate at the time of spend. This makes it practical to capture the business relationship and purpose information the IRS requires without relying on employees to fill out a separate form after the fact.

Extend also integrates directly with accounting platforms including QuickBooks Online, QuickBooks Desktop, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics 365 Business Central, so the expense data — receipts, coding, and all — flows directly into the general ledger without manual rekeying. At audit time, the records are complete, organized, and searchable.

The goal is a system where compliance is the default, not the exception.

Extend helps finance teams capture the right data at the point of spend — so month-end close is faster, and audit prep is just a report, not a fire drill.

This article is for informational purposes only and does not constitute legal or tax advice. Tax rules are subject to change and vary based on individual circumstances. Consult a qualified tax professional for guidance specific to your situation.

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Every finance team has had the conversation: an employee submits an expense report weeks after a trip, the receipts are missing, and no one is quite sure whether a note on a napkin counts. It sounds like an annoyance. But the underlying issue — whether your business can substantiate its expense deductions if the IRS comes asking — is genuinely consequential.

The rules themselves are not especially complicated. The challenge is that they are easy to misremember, frequently oversimplified in casual advice, and almost never built into the moment when an employee is actually handing over a card.

Here is what the IRS actually requires, in plain language, and what finance teams can do to stay confidently prepared.

Under IRC Section 274 and the Treasury Regulations that implement it, a deductible business expense must be supported by "adequate records." The IRS defines this as documentation that establishes five distinct elements:

For most expense categories — travel, meals, lodging, supplies — a receipt from the vendor combined with a brief written note of the business purpose will satisfy all five. The receipt typically covers amount, date, and vendor. The employee's note covers the purpose and, where relevant, who was present.

The business relationship requirement comes up most often for meals and entertainment. If a client dinner is expensed, the name and business relationship of the attendees needs to be documented somewhere — whether that is a notes field in an expense report, a calendar entry, or a follow-up email.

One of the most repeated pieces of expense advice in corporate finance is "you do not need a receipt for anything under $75." It is worth unpacking what this actually means — because it is frequently overstated.

The IRS does provide simplified substantiation options for certain lower-dollar expenses. Under Revenue Procedure 98-25 and the accountable plan regulations, an employer is not required to collect documentary evidence (i.e., a receipt or invoice) for expenses under $75, provided the expense would otherwise qualify and other records are maintained. For lodging, there is no floor — receipts are always required regardless of the amount.

In practice, many finance teams choose to require receipts for all expenses, regardless of amount. This is entirely defensible from an IRS perspective and makes reconciliation significantly cleaner. The $75 threshold is a floor for required documentation, not a permission slip to stop keeping records.

The IRS confirmed in Revenue Procedure 98-25 that electronic records are acceptable, and subsequent guidance has reinforced that emailed receipts, PDF downloads, and scanned images all meet the substantiation standard — as long as the record is accurate, complete, and legible.

What matters is that the digital image or document clearly shows all five required elements. A blurry photo of a receipt where the total is unreadable does not satisfy the requirement. Neither does a partial email confirmation that shows the purchase date but omits the itemization.

The practical implication for finance teams: your receipt management workflow needs to produce complete digital records, not just proof that something was spent. This is where purpose-built tools make a real difference. For example, with a tool like Extend, employees can attach receipts directly to virtual card transactions — and because each virtual card is issued for a specific purpose or vendor, the business-purpose context is often captured before the employee even submits anything.

The general rule is that records supporting a tax return should be kept for at least three years from the date the return was filed. This covers the standard IRS audit window. However, there are circumstances that extend this obligation:

If you substantially understate income — more than 25 percent of gross income is omitted from a return — the IRS has six years to assess additional taxes. If a return is fraudulent or never filed, there is no statute of limitations. For employment tax records specifically, the IRS recommends four years from the date the tax was due or paid, whichever is later.

The practical guidance for most businesses: retain expense records and supporting receipts for at least seven years. It's longer than the standard window, but the storage cost of digital records is low, and it eliminates uncertainty in edge cases.

Beyond the basic receipt rules, three specific expense categories carry their own documentation requirements that finance teams should understand clearly.

An accountable plan is a formal employer reimbursement arrangement that meets IRS criteria: expenses must have a business connection, employees must adequately account for their expenses, and employees must return any excess reimbursement within a reasonable time. When an accountable plan is properly maintained, reimbursements are excluded from employee income and are deductible to the employer. The documentation obligations are the same five-element standard — but the plan structure itself needs to be documented in writing.

Employers who use IRS-approved per diem rates for travel and lodging can simplify documentation significantly. Instead of collecting individual meal and lodging receipts, the employer pays a daily rate, and the employee documents only the time, place, and business purpose of the travel. The per diem rates are set by the General Services Administration (GSA) and vary by location. Using per diems does not eliminate substantiation entirely — it just substitutes a standardized rate for itemized receipt collection.

For employees reimbursed for using personal vehicles, the IRS requires a contemporaneous mileage log that documents the date of the trip, the destination, the business purpose, and the number of miles driven. The standard mileage rate changes annually and is published by the IRS each December.

A few patterns come up repeatedly when businesses face scrutiny over business expense deductions:

Vague business purpose notes: "Client dinner" without the client's name, company, and the business discussed does not fully satisfy the requirement. "Dinner with Sarah Chen, CFO at Meridian Partners — discussed Q3 proposal" does. Specificity matters.

Missing vendor information on informal receipts: A cash register tape that shows only a total and date, with no vendor name or address, is insufficient on its own. A handwritten note accompanying it that adds the vendor details can fill the gap, but the better practice is to ask for a detailed receipt upfront.

Receipts that don't match the card transaction: If an employee submits a receipt for $82 and the card transaction shows $84 (perhaps because of a tip added post-receipt), the documentation needs to account for the discrepancy — usually by noting the tip separately. This is a common issue with restaurant expenses.

Retroactive reconstruction: The IRS specifically disfavors reconstructed records — documentation that was assembled after the fact rather than captured at the time of the expense. Contemporaneous records carry much more weight. This is one of the strongest arguments for capturing expense data at the point of transaction rather than at the end of the month.

Staying compliant with IRS receipt requirements is ultimately an operational challenge, not just a knowledge one. The harder part is building a system where the right documentation gets captured reliably, for every transaction, without putting the burden entirely on employees to remember the rules.

Extend is designed with this in mind.

When a virtual card is created for a specific employee, vendor, or project, the business purpose context is built in from the start. When the card is used, the transaction — including amount, date, and vendor — is recorded automatically. Employees can attach receipts directly to individual transactions via the Extend app or text and email forwarding, so the documentation lives alongside the transaction data rather than in a separate system.

For expense data beyond the basic five elements, Extend's Additional Fields for Expense Capture lets finance teams define custom fields — project codes, department tags, client names, or any other data point the business tracks — that populate at the time of spend. This makes it practical to capture the business relationship and purpose information the IRS requires without relying on employees to fill out a separate form after the fact.

Extend also integrates directly with accounting platforms including QuickBooks Online, QuickBooks Desktop, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics 365 Business Central, so the expense data — receipts, coding, and all — flows directly into the general ledger without manual rekeying. At audit time, the records are complete, organized, and searchable.

The goal is a system where compliance is the default, not the exception.

Extend helps finance teams capture the right data at the point of spend — so month-end close is faster, and audit prep is just a report, not a fire drill.

This article is for informational purposes only and does not constitute legal or tax advice. Tax rules are subject to change and vary based on individual circumstances. Consult a qualified tax professional for guidance specific to your situation.

Every finance team has had the conversation: an employee submits an expense report weeks after a trip, the receipts are missing, and no one is quite sure whether a note on a napkin counts. It sounds like an annoyance. But the underlying issue — whether your business can substantiate its expense deductions if the IRS comes asking — is genuinely consequential.

The rules themselves are not especially complicated. The challenge is that they are easy to misremember, frequently oversimplified in casual advice, and almost never built into the moment when an employee is actually handing over a card.

Here is what the IRS actually requires, in plain language, and what finance teams can do to stay confidently prepared.

Under IRC Section 274 and the Treasury Regulations that implement it, a deductible business expense must be supported by "adequate records." The IRS defines this as documentation that establishes five distinct elements:

For most expense categories — travel, meals, lodging, supplies — a receipt from the vendor combined with a brief written note of the business purpose will satisfy all five. The receipt typically covers amount, date, and vendor. The employee's note covers the purpose and, where relevant, who was present.

The business relationship requirement comes up most often for meals and entertainment. If a client dinner is expensed, the name and business relationship of the attendees needs to be documented somewhere — whether that is a notes field in an expense report, a calendar entry, or a follow-up email.

One of the most repeated pieces of expense advice in corporate finance is "you do not need a receipt for anything under $75." It is worth unpacking what this actually means — because it is frequently overstated.

The IRS does provide simplified substantiation options for certain lower-dollar expenses. Under Revenue Procedure 98-25 and the accountable plan regulations, an employer is not required to collect documentary evidence (i.e., a receipt or invoice) for expenses under $75, provided the expense would otherwise qualify and other records are maintained. For lodging, there is no floor — receipts are always required regardless of the amount.

In practice, many finance teams choose to require receipts for all expenses, regardless of amount. This is entirely defensible from an IRS perspective and makes reconciliation significantly cleaner. The $75 threshold is a floor for required documentation, not a permission slip to stop keeping records.

The IRS confirmed in Revenue Procedure 98-25 that electronic records are acceptable, and subsequent guidance has reinforced that emailed receipts, PDF downloads, and scanned images all meet the substantiation standard — as long as the record is accurate, complete, and legible.

What matters is that the digital image or document clearly shows all five required elements. A blurry photo of a receipt where the total is unreadable does not satisfy the requirement. Neither does a partial email confirmation that shows the purchase date but omits the itemization.

The practical implication for finance teams: your receipt management workflow needs to produce complete digital records, not just proof that something was spent. This is where purpose-built tools make a real difference. For example, with a tool like Extend, employees can attach receipts directly to virtual card transactions — and because each virtual card is issued for a specific purpose or vendor, the business-purpose context is often captured before the employee even submits anything.

The general rule is that records supporting a tax return should be kept for at least three years from the date the return was filed. This covers the standard IRS audit window. However, there are circumstances that extend this obligation:

If you substantially understate income — more than 25 percent of gross income is omitted from a return — the IRS has six years to assess additional taxes. If a return is fraudulent or never filed, there is no statute of limitations. For employment tax records specifically, the IRS recommends four years from the date the tax was due or paid, whichever is later.

The practical guidance for most businesses: retain expense records and supporting receipts for at least seven years. It's longer than the standard window, but the storage cost of digital records is low, and it eliminates uncertainty in edge cases.

Beyond the basic receipt rules, three specific expense categories carry their own documentation requirements that finance teams should understand clearly.

An accountable plan is a formal employer reimbursement arrangement that meets IRS criteria: expenses must have a business connection, employees must adequately account for their expenses, and employees must return any excess reimbursement within a reasonable time. When an accountable plan is properly maintained, reimbursements are excluded from employee income and are deductible to the employer. The documentation obligations are the same five-element standard — but the plan structure itself needs to be documented in writing.

Employers who use IRS-approved per diem rates for travel and lodging can simplify documentation significantly. Instead of collecting individual meal and lodging receipts, the employer pays a daily rate, and the employee documents only the time, place, and business purpose of the travel. The per diem rates are set by the General Services Administration (GSA) and vary by location. Using per diems does not eliminate substantiation entirely — it just substitutes a standardized rate for itemized receipt collection.

For employees reimbursed for using personal vehicles, the IRS requires a contemporaneous mileage log that documents the date of the trip, the destination, the business purpose, and the number of miles driven. The standard mileage rate changes annually and is published by the IRS each December.

A few patterns come up repeatedly when businesses face scrutiny over business expense deductions:

Vague business purpose notes: "Client dinner" without the client's name, company, and the business discussed does not fully satisfy the requirement. "Dinner with Sarah Chen, CFO at Meridian Partners — discussed Q3 proposal" does. Specificity matters.

Missing vendor information on informal receipts: A cash register tape that shows only a total and date, with no vendor name or address, is insufficient on its own. A handwritten note accompanying it that adds the vendor details can fill the gap, but the better practice is to ask for a detailed receipt upfront.

Receipts that don't match the card transaction: If an employee submits a receipt for $82 and the card transaction shows $84 (perhaps because of a tip added post-receipt), the documentation needs to account for the discrepancy — usually by noting the tip separately. This is a common issue with restaurant expenses.

Retroactive reconstruction: The IRS specifically disfavors reconstructed records — documentation that was assembled after the fact rather than captured at the time of the expense. Contemporaneous records carry much more weight. This is one of the strongest arguments for capturing expense data at the point of transaction rather than at the end of the month.

Staying compliant with IRS receipt requirements is ultimately an operational challenge, not just a knowledge one. The harder part is building a system where the right documentation gets captured reliably, for every transaction, without putting the burden entirely on employees to remember the rules.

Extend is designed with this in mind.

When a virtual card is created for a specific employee, vendor, or project, the business purpose context is built in from the start. When the card is used, the transaction — including amount, date, and vendor — is recorded automatically. Employees can attach receipts directly to individual transactions via the Extend app or text and email forwarding, so the documentation lives alongside the transaction data rather than in a separate system.

For expense data beyond the basic five elements, Extend's Additional Fields for Expense Capture lets finance teams define custom fields — project codes, department tags, client names, or any other data point the business tracks — that populate at the time of spend. This makes it practical to capture the business relationship and purpose information the IRS requires without relying on employees to fill out a separate form after the fact.

Extend also integrates directly with accounting platforms including QuickBooks Online, QuickBooks Desktop, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics 365 Business Central, so the expense data — receipts, coding, and all — flows directly into the general ledger without manual rekeying. At audit time, the records are complete, organized, and searchable.

The goal is a system where compliance is the default, not the exception.

Extend helps finance teams capture the right data at the point of spend — so month-end close is faster, and audit prep is just a report, not a fire drill.

This article is for informational purposes only and does not constitute legal or tax advice. Tax rules are subject to change and vary based on individual circumstances. Consult a qualified tax professional for guidance specific to your situation.

Every finance team has had the conversation: an employee submits an expense report weeks after a trip, the receipts are missing, and no one is quite sure whether a note on a napkin counts. It sounds like an annoyance. But the underlying issue — whether your business can substantiate its expense deductions if the IRS comes asking — is genuinely consequential.

The rules themselves are not especially complicated. The challenge is that they are easy to misremember, frequently oversimplified in casual advice, and almost never built into the moment when an employee is actually handing over a card.

Here is what the IRS actually requires, in plain language, and what finance teams can do to stay confidently prepared.

Under IRC Section 274 and the Treasury Regulations that implement it, a deductible business expense must be supported by "adequate records." The IRS defines this as documentation that establishes five distinct elements:

For most expense categories — travel, meals, lodging, supplies — a receipt from the vendor combined with a brief written note of the business purpose will satisfy all five. The receipt typically covers amount, date, and vendor. The employee's note covers the purpose and, where relevant, who was present.

The business relationship requirement comes up most often for meals and entertainment. If a client dinner is expensed, the name and business relationship of the attendees needs to be documented somewhere — whether that is a notes field in an expense report, a calendar entry, or a follow-up email.

One of the most repeated pieces of expense advice in corporate finance is "you do not need a receipt for anything under $75." It is worth unpacking what this actually means — because it is frequently overstated.

The IRS does provide simplified substantiation options for certain lower-dollar expenses. Under Revenue Procedure 98-25 and the accountable plan regulations, an employer is not required to collect documentary evidence (i.e., a receipt or invoice) for expenses under $75, provided the expense would otherwise qualify and other records are maintained. For lodging, there is no floor — receipts are always required regardless of the amount.

In practice, many finance teams choose to require receipts for all expenses, regardless of amount. This is entirely defensible from an IRS perspective and makes reconciliation significantly cleaner. The $75 threshold is a floor for required documentation, not a permission slip to stop keeping records.

The IRS confirmed in Revenue Procedure 98-25 that electronic records are acceptable, and subsequent guidance has reinforced that emailed receipts, PDF downloads, and scanned images all meet the substantiation standard — as long as the record is accurate, complete, and legible.

What matters is that the digital image or document clearly shows all five required elements. A blurry photo of a receipt where the total is unreadable does not satisfy the requirement. Neither does a partial email confirmation that shows the purchase date but omits the itemization.

The practical implication for finance teams: your receipt management workflow needs to produce complete digital records, not just proof that something was spent. This is where purpose-built tools make a real difference. For example, with a tool like Extend, employees can attach receipts directly to virtual card transactions — and because each virtual card is issued for a specific purpose or vendor, the business-purpose context is often captured before the employee even submits anything.

The general rule is that records supporting a tax return should be kept for at least three years from the date the return was filed. This covers the standard IRS audit window. However, there are circumstances that extend this obligation:

If you substantially understate income — more than 25 percent of gross income is omitted from a return — the IRS has six years to assess additional taxes. If a return is fraudulent or never filed, there is no statute of limitations. For employment tax records specifically, the IRS recommends four years from the date the tax was due or paid, whichever is later.

The practical guidance for most businesses: retain expense records and supporting receipts for at least seven years. It's longer than the standard window, but the storage cost of digital records is low, and it eliminates uncertainty in edge cases.

Beyond the basic receipt rules, three specific expense categories carry their own documentation requirements that finance teams should understand clearly.

An accountable plan is a formal employer reimbursement arrangement that meets IRS criteria: expenses must have a business connection, employees must adequately account for their expenses, and employees must return any excess reimbursement within a reasonable time. When an accountable plan is properly maintained, reimbursements are excluded from employee income and are deductible to the employer. The documentation obligations are the same five-element standard — but the plan structure itself needs to be documented in writing.

Employers who use IRS-approved per diem rates for travel and lodging can simplify documentation significantly. Instead of collecting individual meal and lodging receipts, the employer pays a daily rate, and the employee documents only the time, place, and business purpose of the travel. The per diem rates are set by the General Services Administration (GSA) and vary by location. Using per diems does not eliminate substantiation entirely — it just substitutes a standardized rate for itemized receipt collection.

For employees reimbursed for using personal vehicles, the IRS requires a contemporaneous mileage log that documents the date of the trip, the destination, the business purpose, and the number of miles driven. The standard mileage rate changes annually and is published by the IRS each December.

A few patterns come up repeatedly when businesses face scrutiny over business expense deductions:

Vague business purpose notes: "Client dinner" without the client's name, company, and the business discussed does not fully satisfy the requirement. "Dinner with Sarah Chen, CFO at Meridian Partners — discussed Q3 proposal" does. Specificity matters.

Missing vendor information on informal receipts: A cash register tape that shows only a total and date, with no vendor name or address, is insufficient on its own. A handwritten note accompanying it that adds the vendor details can fill the gap, but the better practice is to ask for a detailed receipt upfront.

Receipts that don't match the card transaction: If an employee submits a receipt for $82 and the card transaction shows $84 (perhaps because of a tip added post-receipt), the documentation needs to account for the discrepancy — usually by noting the tip separately. This is a common issue with restaurant expenses.

Retroactive reconstruction: The IRS specifically disfavors reconstructed records — documentation that was assembled after the fact rather than captured at the time of the expense. Contemporaneous records carry much more weight. This is one of the strongest arguments for capturing expense data at the point of transaction rather than at the end of the month.

Staying compliant with IRS receipt requirements is ultimately an operational challenge, not just a knowledge one. The harder part is building a system where the right documentation gets captured reliably, for every transaction, without putting the burden entirely on employees to remember the rules.

Extend is designed with this in mind.

When a virtual card is created for a specific employee, vendor, or project, the business purpose context is built in from the start. When the card is used, the transaction — including amount, date, and vendor — is recorded automatically. Employees can attach receipts directly to individual transactions via the Extend app or text and email forwarding, so the documentation lives alongside the transaction data rather than in a separate system.

For expense data beyond the basic five elements, Extend's Additional Fields for Expense Capture lets finance teams define custom fields — project codes, department tags, client names, or any other data point the business tracks — that populate at the time of spend. This makes it practical to capture the business relationship and purpose information the IRS requires without relying on employees to fill out a separate form after the fact.

Extend also integrates directly with accounting platforms including QuickBooks Online, QuickBooks Desktop, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics 365 Business Central, so the expense data — receipts, coding, and all — flows directly into the general ledger without manual rekeying. At audit time, the records are complete, organized, and searchable.

The goal is a system where compliance is the default, not the exception.

Extend helps finance teams capture the right data at the point of spend — so month-end close is faster, and audit prep is just a report, not a fire drill.

This article is for informational purposes only and does not constitute legal or tax advice. Tax rules are subject to change and vary based on individual circumstances. Consult a qualified tax professional for guidance specific to your situation.

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)